Insurance Coverage For Emergency Plumbing Damage

Insurance coverage for emergency plumbing damage: an overview

When a pipe bursts in the middle of the night or a water heater fails, the disruption is immediate and costly. Understanding insurance coverage for emergency plumbing damage can mean the difference between an insurer paying for repairs and a homeowner absorbing most of the cost. Chicago Pipe Essentials helps homeowners navigate these situations, clarifying what policies typically cover and what documentation insurers will want. For immediate guidance on filing a claim and documenting losses, call 312-555-4821.

Emergency plumbing claims sit at the intersection of property insurance, policy language, and prompt action. Insurance contracts use specific terms-like sudden and accidental versus gradual damage-to determine coverage. Knowing your policy's ins and outs, what mitigation steps to take, and how to create a clear, time-stamped record improves your chances of a fair settlement.

Understanding basic policy coverages and exclusions

Most homeowners insurance policies provide some protection for sudden plumbing-related events. Standard policies (for example HO-3 forms) commonly cover water damage resulting from a sudden, accidental discharge-such as a burst supply line or a broken appliance hose-subject to policy limits and deductibles. However, not all water-related losses are treated the same, and several important exclusions often apply.

Common coverages include immediate clean-up and repair of structural damage, replacement of damaged personal property (subject to limits), and additional living expenses if your home is temporarily uninhabitable. On the exclusions side, insurers regularly deny claims for losses caused by lack of maintenance, long-term leaks, and flood or groundwater intrusion unless specific endorsements are in place.

- Typical coverages: sudden pipe bursts, appliance failures causing discharge, and some sewer back-ups (when endorsed).

- Typical exclusions: wear and tear, poor maintenance, gradual leaks, and flood-related damage without a separate flood policy.

- Common endorsements: water backup/sewer backup, service line coverage, and equipment breakdown coverage for appliances and systems.

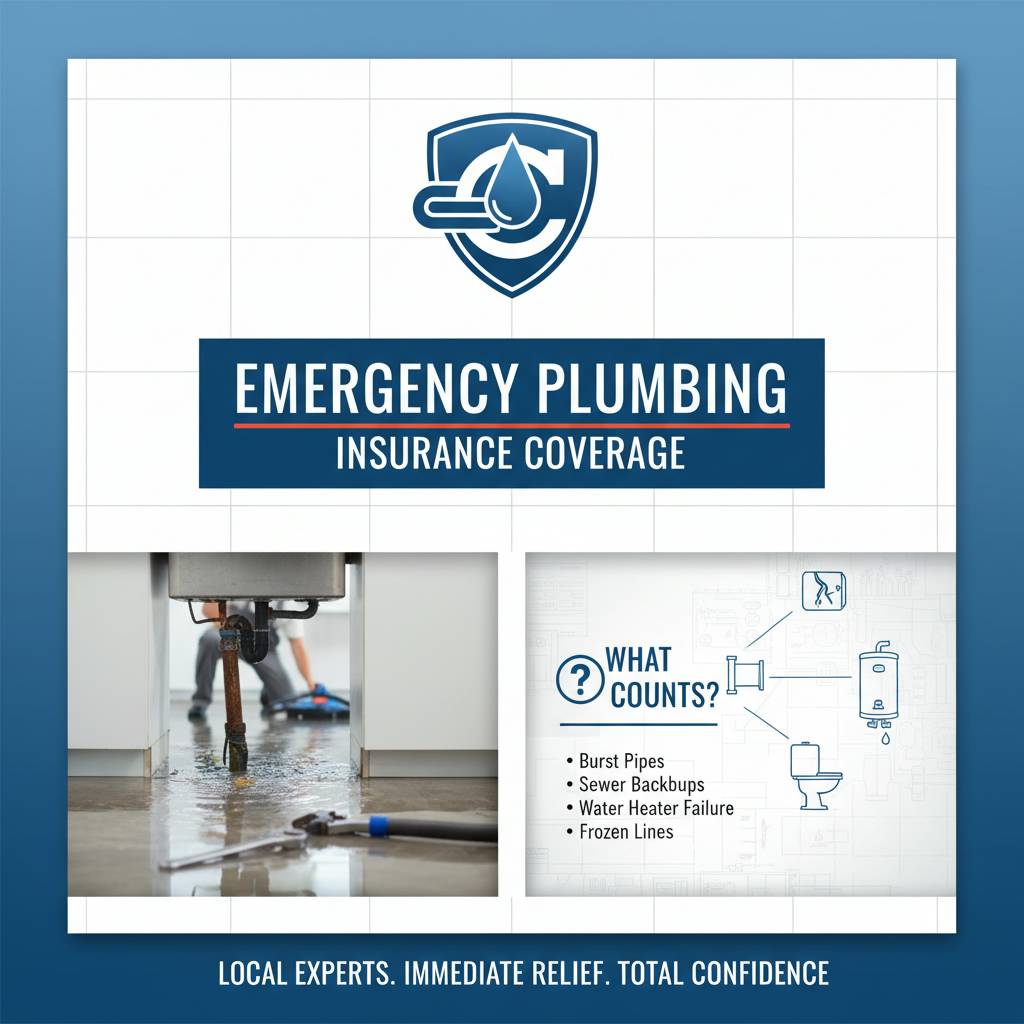

What counts as an emergency plumbing event?

Insurers generally distinguish emergencies from routine maintenance problems by focusing on the speed and severity of the event. An emergency plumbing event is usually defined as a sudden, accidental occurrence that causes unexpected water discharge or sewage backup and requires immediate action to prevent further damage. Examples include a ruptured supply line, a failed water heater, an overflowing washer due to a broken hose, or a tree root causing an abrupt sewer line collapse.

Insurers generally distinguish emergencies from routine maintenance problems by focusing on the speed and severity of the event. An emergency plumbing event is usually defined as a sudden, accidental occurrence that causes unexpected water discharge or sewage backup and requires immediate action to prevent further damage. Examples include a ruptured supply line, a failed water heater, an overflowing washer due to a broken hose, or a tree root causing an abrupt sewer line collapse.

Events that occur gradually-such as slow leaks that develop over months due to corrosion-are often classified as maintenance issues and are therefore excluded. For homeowners, the practical takeaway is to treat anything that causes rapid water flow or visible flooding as an emergency: stop the source if possible, document the scene, and contact professionals quickly.

Immediate steps to take during an emergency

When an emergency plumbing incident occurs, follow a clear, safety-first checklist. Shut off the main water valve if you can do so safely. Turn off electricity to affected areas if water has reached outlets or electrical devices. Take time-stamped photos and short video clips of the damage before moving items. Call a licensed plumber for an emergency mitigation repair and retain receipts for labor and materials-insurers typically look for evidence that you tried to limit further loss.

- Locate and shut off water source (main shutoff or localized valve).

- Ensure electrical systems are safe; shut power to affected circuits if necessary.

- Document damage with photos/videos and notes about timing and circumstances.

- Contact an emergency plumber or mitigation company and keep all receipts.

- Notify your insurance company as soon as you can-late notice risks denial.

Documentation insurers expect and how to present it

Documentation is the backbone of every successful claim for insurance coverage for emergency plumbing damage. Insurers evaluate both the cause and the extent of loss, so you'll need evidence that an abrupt, covered event occurred and that you took reasonable steps to mitigate further damage. Organized, chronological documentation reduces friction during the claim review and helps you maintain credibility in discussions with adjusters.

Key pieces of evidence include dated photos and videos, a written timeline of events, emergency repair invoices, mitigation or drying company reports, plumber diagnosis reports, and receipts for temporary housing and replacement items. If a contractor recommends a permanent repair, keep that written estimate. If the cause might be due to external factors-like a municipal sewer issue-obtain a formal report from the utility or municipal authority whenever possible.

- Photos and videos with timestamps showing the damage and the source (if visible).

- Emergency service invoices and repair permits, if issued.

- Plumber's diagnosis describing the sudden cause (e.g., pipe burst due to freezing).

- Receipts for mitigation, temporary repairs, and any immediate replacement of essentials.

- A log of communications with the insurer and contractor estimates for permanent repairs.

Filing the claim: timelines, adjusters, and communication

Start your claim as soon as reasonably possible. Most policies require prompt notice; failing to notify your insurer can lead to partial or full denial. When you call your insurer, provide a concise account of the event, share the immediate actions you took to mitigate damage, and ask for the claim number and the expected next steps. Save the name and contact information of the claims representative assigned to your case.

Start your claim as soon as reasonably possible. Most policies require prompt notice; failing to notify your insurer can lead to partial or full denial. When you call your insurer, provide a concise account of the event, share the immediate actions you took to mitigate damage, and ask for the claim number and the expected next steps. Save the name and contact information of the claims representative assigned to your case.

An adjuster will likely inspect the property to assess damage and cause. Be prepared to walk the adjuster through your documentation, show photos and invoices, and point out where the incident originated. If temporary emergency repairs were made to stop ongoing damage, keep receipts and before/after photos. Keep a written record of each conversation with dates, times, and names to avoid misunderstandings.

Working effectively with adjusters and contractors

Adjusters evaluate coverage under the policy language and estimate costs; contractors estimate repair costs and perform work. To avoid conflicts, obtain at least one independent estimate for larger repairs and share all estimates with your insurer. If the insurer insists on using a preferred contractor, you retain the right to hire your own licensed contractor; negotiation about scope and price is common. If disagreements persist, consider a second opinion from an independent public adjuster or a construction professional.

Common pitfalls and denial reasons (and how to avoid them)

Denials commonly occur when insurers conclude that damage resulted from long-term neglect, wear and tear, or an excluded peril. Homeowners often underestimate how important timely mitigation and clear documentation are. Examples include failing to repair a slow leak until significant damage occurs, not obtaining professional mitigation services, or failing to preserve evidence because belongings were discarded prematurely.

Denials commonly occur when insurers conclude that damage resulted from long-term neglect, wear and tear, or an excluded peril. Homeowners often underestimate how important timely mitigation and clear documentation are. Examples include failing to repair a slow leak until significant damage occurs, not obtaining professional mitigation services, or failing to preserve evidence because belongings were discarded prematurely.

To reduce the risk of denial, read your policy proactively so you understand covered perils and endorsements. Purchase appropriate endorsements if your home is at risk for sewer backup or if your plumbing systems are older. Always act quickly to stop damage, document the scene thoroughly before moving items when safe to do so, and retain receipts for emergency work. If you suspect the insurer's interpretation is unfair, ask for the denial in writing and request a detailed explanation. This helps if you seek mediation, appraisal, or legal advice later.

Case studies: practical examples of coverage outcomes

Case study 1: Burst pipe due to freezing. A homeowner experienced a sudden main supply line rupture during a cold snap. They immediately shut off the main, took time-stamped photos, hired an emergency plumber, and documented all communications and receipts. The insurance company accepted the claim as sudden and accidental and covered structural repairs and content replacement minus the deductible. Quick mitigation and clear documentation were decisive.

Case study 1: Burst pipe due to freezing. A homeowner experienced a sudden main supply line rupture during a cold snap. They immediately shut off the main, took time-stamped photos, hired an emergency plumber, and documented all communications and receipts. The insurance company accepted the claim as sudden and accidental and covered structural repairs and content replacement minus the deductible. Quick mitigation and clear documentation were decisive.

Case study 2: Slow leak and a denied claim. Another homeowner had persistent, slow leakage under a bathroom vanity for months. Despite visible staining and increasing mold, the leak wasn't repaired promptly. When the homeowner finally filed a claim for extensive rot and mold remediation, the insurer denied coverage, citing neglect and lack of maintenance. This example highlights how gradual damage is treated differently and why routine maintenance matters.

When to seek help from professionals

There are times when professional advocacy can be valuable. If coverage is unclear, a denial feels unjustified, or the insurer's estimated payment is far below contractor bids, consult a public adjuster or an attorney with insurance claim experience. A licensed public adjuster can review your claim, document losses comprehensively, and negotiate with the insurer on your behalf. Legal counsel is advisable when there are disputes about policy interpretation or bad-faith handling.

There are times when professional advocacy can be valuable. If coverage is unclear, a denial feels unjustified, or the insurer's estimated payment is far below contractor bids, consult a public adjuster or an attorney with insurance claim experience. A licensed public adjuster can review your claim, document losses comprehensively, and negotiate with the insurer on your behalf. Legal counsel is advisable when there are disputes about policy interpretation or bad-faith handling.

Chicago Pipe Essentials can help you evaluate whether a denial was appropriate and advise steps to document and present additional evidence. If you prefer a hands-on partner, we can assist with organizing records, preparing the timeline of events, and identifying contractors skilled at preserving the documentation insurers need.

Practical tips to protect your home and coverage going forward

Prevention and preparedness are as important as documentation. Schedule seasonal maintenance for pipes and appliances, insulate exposed plumbing, and install automatic shut-off valves or leak-detection systems to limit future losses. Review your homeowners policy annually-especially if your plumbing systems are older-and consider endorsements for sewer backup or service line coverage if your risk profile suggests them.

Keep a digital folder or cloud storage with appliance manuals, service records, and photos of key systems in your home so you can quickly demonstrate regular upkeep. Simple, proactive steps often make the difference between a covered emergency and an uncovered maintenance issue.

Frequently asked questions

Does homeowners insurance cover sewer backups?

Not usually-sewer backups are commonly excluded from standard policies, but they can be added with a water backup or sewer backup endorsement. If you live in an area with older sewer lines or frequent backups, securing that endorsement can be a low-cost way to gain protection.

Are burst pipes always covered?

Coverage depends on cause. Pipes that burst suddenly due to freezing, accidental impact, or other sudden events are typically covered. Pipes that fail because of long-term corrosion or lack of maintenance are often excluded. Timely mitigation and documentation help prove a sudden event occurred.

What about mold resulting from plumbing damage?

Mold remediation is treated case-by-case. If mold results from a covered peril and you reported and mitigated the issue promptly, insurers may cover remediation up to policy limits. If mold stems from a long-term, unaddressed leak, coverage is less likely.

How Chicago Pipe Essentials supports homeowners through the recovery process

At Chicago Pipe Essentials, we guide homeowners through every step-from immediate mitigation advice to preparing a thorough claims package. Our team helps you understand which parts of your loss are most likely covered, compiles the documentation insurers request, and coordinates with contractors and adjusters to keep the process moving. We also offer practical guidance on minimizing further damage, preserving evidence, and completing repairs efficiently.

If you prefer, we can perform an initial case review and help you decide whether to submit a claim, seek an endorsement, or pursue independent estimates. CPE and our team provide calm, evidence-based recommendations so you know what to expect and how to preserve your rights under the policy.

Call now: For immediate assistance and claim guidance, contact Chicago Pipe Essentials at 312-555-4821. We can help you take the right first steps and organize the documentation insurers need.

Need a quick checklist? We'll send a simple emergency documentation checklist and sample language for notifying your insurer when you call, so you can act with confidence and clarity during a stressful situation.

When emergency plumbing damage occurs, timely action and good documentation are the keys to a successful outcome. Chicago Pipe Essentials is ready to support you through mitigation, claim filing, and the recovery process-call 312-555-4821 to get a clear plan and personal assistance. We look forward to helping you put your home back together and navigate insurance coverage for emergency plumbing damage with confidence.